menu

menu

Our latest reading of director confidence is double-sided—with a bit of good news and a bit of not-so-good news.

Starting with the not-so-good news:

On the good news front: this downgrading of conditions appears to be more of an adjustment rather than a dismal outlook. Here’s why:

The caveat: the upcoming presidential election in November.

The 140 public company board members we polled August 12-15 as part of our Director Confidence Index survey conducted in partnership with Diligent Institute say that while cooling inflation and an all-but-confirmed September interest rate cut are good indicators for the U.S. economy, the outcome of the upcoming presidential election is causing a great deal of uncertainty.

“It really all depends on the election outcome,” said one participating board member, echoing many others whose forecast for business in the year ahead came with a similar caveat.

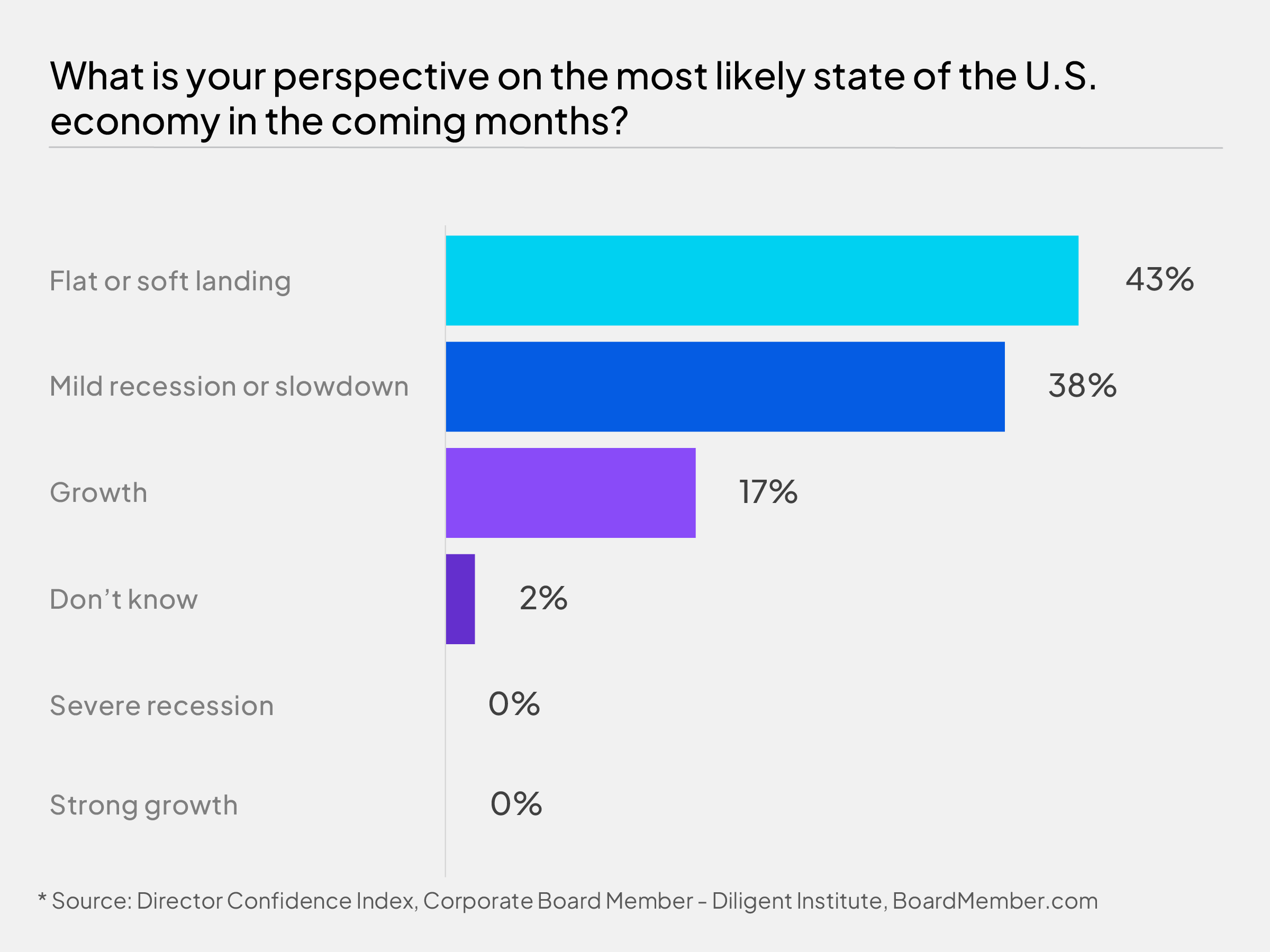

Overall, only 38 percent expect a mild recession or slowdown in the coming months (vs. 60 percent of CEOs, when asked by sister publication Chief Executive—though in all fairness, CEOs were polled in the midst of the market pullback while our director survey fielded during the upswing that followed). Not a single director said they expected anything more severe than a slowdown.

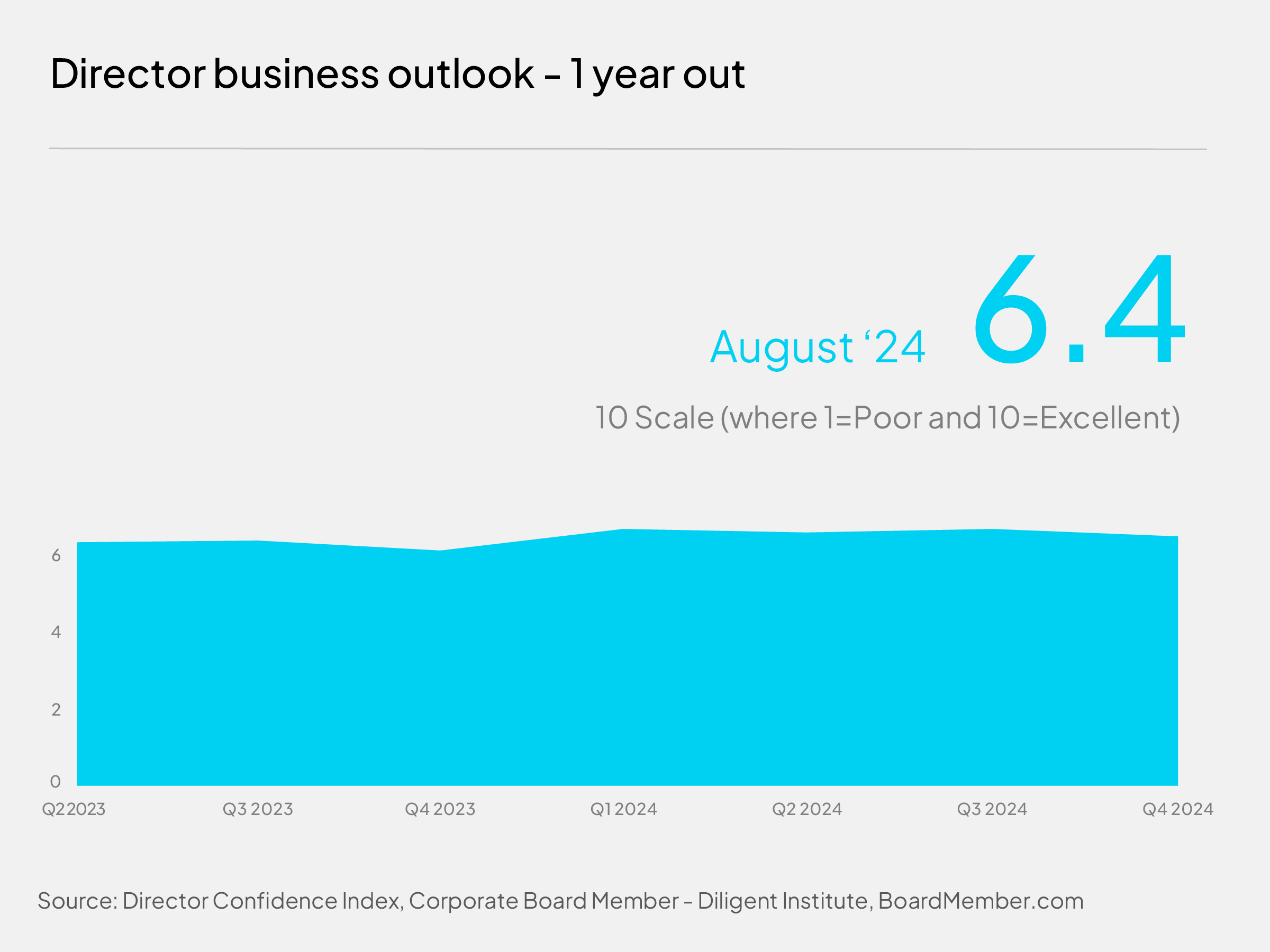

And the proportion of directors who expect conditions to improve in the next 12 months climbed 2 points, from 40 percent in July to 42 percent this August, while those who expect conditions to deteriorate declined by the same margin, to 26 percent from 28 percent. The remaining 32 percent expect conditions to remain the same.

When asked about how this is affecting their forecasts for their companies, 74 percent said despite the uncertainty, they still anticipate their company’s revenue to increase over the next 12 months.

That proportion is down from 79 percent in late June/early July, but it remains relatively high when compared to prior years. In 2023, the average proportion of directors who, on a monthly basis, said they expected to increase revenues over a 12-month period was 67 percent. In 2022, that number was 72 percent. In contrast, so far in 2024, that average beats both years, at 77 percent.

The only year (since we started fielding this survey in the fall of 2020) that has found more directors bullish on revenue increases is 2021, when 87 percent of directors on average each month said they expected revenues to increase in the year ahead—in a highly hopeful post-pandemic environment.

When asked about profitability, 70 percent of directors in our August poll said they expected profits to increase over the next 12 months (vs. 69 percent in July). Our year-over-year comparison finds a similar pattern: 71 percent have forecasted increasing profits so far in 2024 (on average, each month), vs. 60 percent in 2023, 63 percent in 2022 and 81 percent in 2021.

In terms of capital expenditures, 42 percent said they plan to increase expenditures over the coming months—down 4 percent from the 44 percent who said the same in late June/early July. This remains a relatively high proportion when looking at our historical data: 22 percent higher than where it was at this time last year and the second-highest level (after July 2024) since April 2022.